As a result of lockdowns due to the Covid-19 pandemic, online shopping increased by 24.1% from 2019 to 2020. Consumers worldwide spend approximately $4.29 trillion online (Young, 2021). As e-commerce has grown more popular so has the payment options and new innovative alternatives appears.

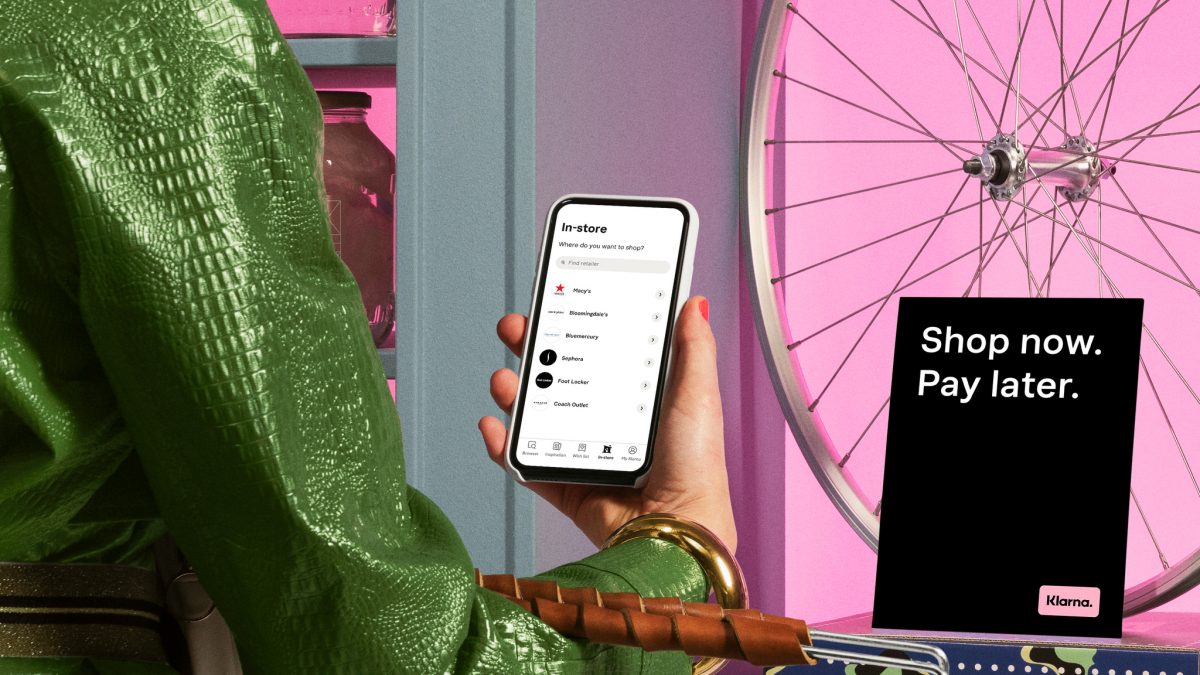

Digital innovation in payment methods has revolutionized the online shopping experience in many ways, and the world of banking could be expecting a radical change in consumer behavior. An example of an alternative is the Open Banking payment solution is Klarna (Meyers, 2021). Klarna was founded in 2005 and is a Swedish fin-tech platform with the slogan: Shop now. Pay Later. Klarna has 200,000 retail partners and processes more than 150 million transactions a year (Silicon Canals, 2021). But how did Klarna become so popular? And is their model a trend in payment methods?

The idea of Klarna is to offer consumers a more transparent, convenient and flexible way of shopping and paying that goes beyond the traditional credit and debit cards. Klarna is offering its consumers to shop the items they desire and wait with the payment until 14 or 30 days. This gives the consumer time to try the product and decide if they want to keep it or return it and is thereby a flexible option that decreases personal money transactions. There are no extra fees or interest rates for postponing the payment creating great value and flexibility for consumers (Meyers, 2021; Silicon Canals, 2021). Especially for the generations Millennials’ and Gen-Z it is convenient to use Klarna or other payment methods such as Afterpay. This payment method might have the effect of making consumers buy more possibly generating even more growth in the future of e-commerce (Subin, 2021).

References:

Meyers, T. (2021) Klarna Discusses Shifting Winds in Retail, Emerging Customer Trends. WWD.com. Retrieved from: https://wwd.com/business-news/business-features/klarna-shifting-retail-customer-trends-1234783157/

Silicon Canals (2021) Sweden fintech Klarna expands its Open Banking solutions in these 8 European countries. SiliconCanals.com. Retrieved from: https://siliconcanals.com/news/startups/fintech/klarna-expands-its-open-banking-solutions/

Subin, S. (2021) Why millennials and genZs are jumping on the buy now, pay later trend. CNBC.com. Retrieved from: https://www.cnbc.com/2021/08/07/why-millennials-and-gen-zs-are-jumping-on-the-buy-now-pay-later-trend.html

Young, J. (2021) Global online sales reach nearly $4.29 trillion in 2020. DigitalCommerce360.com. Retrieved from: https://www.digitalcommerce360.com/article/global-ecommerce-sales/

Very informative and up-to-date article! Indeed the COVID-19 accelerated online shopping and in some circumstances it replaced the traditional way of buying but i was not even aware of this fin-tech. The way they operate the payment method is very innovative and combats an issue faced by customers when buying online, which is not having the opportunity to try and feel the item. However a rising question could be what actions have they taken in order to encounter fraudulent customers if they have any?

Very interesting article Mia! I was surprised to read that Klarna was already founded back in 2005, since nowadays it’s such a common paying method. I often use Klarna myself, so I’m not amazed by the fact that the company has more than 200,000 retail partners. The company offers many benefits if you compare it to traditional backing. One of the benefits which in my opinion is extra striking, is that no registration is required. Moreover, the merchant has no access to confidential online banking details. Exceptional is that the company lets you try before you commit to buying all products; a mindset that especially Gen Z and millennials like. But if you don’t pay in time, it dóes affect the customer’s credit score and the company passes the account to debt collection agencies. So, I’m curious, do you think that Klarna’s motto “buy now, pay later” is actually a debt trap?

Interesting article Mia! As Daphne mentioned, I was also surprised that Klarna was already founded in 2005. I had never noticed its existence before recent years. In addition to fraudulent customers and trapping customers into debt, I was wondering how will deal with returns from online sales. Currently, returns of online sales already have a serious impact on the company’s profit. Some companies charge consumers in order to return their merchandise. Other companies see free return shipping as an investment that pays off with long-term sales (Hausman, 2012). If every customer adopts Klarna as their payment method, orders increase, and simultaneously returns increase. Do you think that free return policy will still be beneficial?

Great article! As a Swede it’s fun to see that Klarna is being becoming more well known internationally.

Adding to what you and Shirley wrote regarding increased sales and returns, I think another interesting factor to consider is the environmental impact of this. Several reports have come out stating that the majority of clothing items that are returned to some brands are thrown away due to the high costs of processing returns. With free shipping and returns, and payments services like Klarna, making it easier than ever to order online and try things before committing, I’m curious to see if this will be a sustainable model in the future. It will also be interesting to see how Klarna would adapt to changing return policies.