5/5 (1) The advent of the internet has significantly “reduced the time and cost of processing and communicating information” (Malone, Yates & Benjamin, 1987) and, in doing so, ushered in a new era – one in which tech giants dominate the global economy. Over the past two decades, companies like Apple, Alibaba, Facebook, Google and Amazon have silently grown their multinational influence to gargantuan proportions. While top-ranking executives at traditional companies are left in awe and feel ‘platform envy’ at the mere mention these platform giants (Schrage, 2017), small retailers have desperately been crying out for help only to be drowned – and forced out of business – by smarter competitors. The subtleties of modern-day technology empires make it difficult to notice how they have slowly begun to penetrate every aspect of everyday life. With giant, legacy retailers struggling to survive – the latest example of which is Toys ‘R Us filing for bankruptcy (Gensler, 2017) – governments are trying to fight back by slamming companies like Amazon with ‘back taxes’ of hundreds of millions of euros (Finimize, 2017a). But how exactly are these giants conquering the world? Let’s try to answer this question by taking a closer look at Amazon.

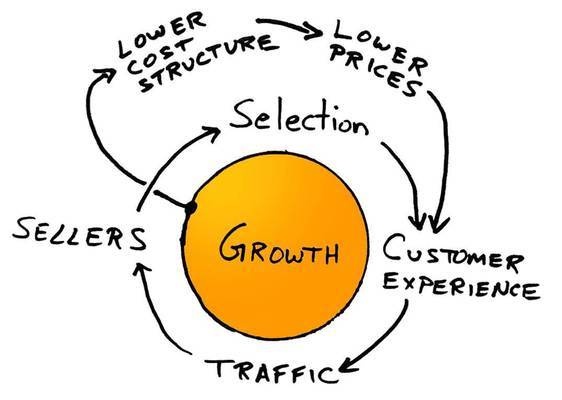

It all starts with Amazon’s infamous flywheel, which has ironically been named “The Virtuous Cycle” (Seely, 2017). Reflecting on the discovery of the flywheel in 2001, Brad Stone writes (Stone, 2017):

“Bezos and his lieutenants sketched their own virtuous cycle, which they believe powered their business. It went something like this: Lower prices led to more customer visits. More customers increased the volume of sales and attracted more commission-paying third party sellers to the site. That allowed Amazon to get more out of fixed costs like the fulfillment centers and the servers they needed to run the website. This greater efficiency then enabled it to lower prices further. Feed any part of this flywheel… and it should accelerate the loop. Amazon executives were elated… after five years, they finally understood their business.”

Indeed, the flywheel effect seems rather straightforward and is a perfect example of how dominant platforms are in a perfect position to leverage network effects; Amazon has become a master at this. It very hard to beat a non-profit business. Other companies have to make a profit or their investors will be angry. Jeff Bezos has successfully made people want to support a company that does not have to make a profit, and that is an incredible business advantage. It has enabled Amazon to become an unimaginably large company unhindered by Christensen’s “innovator’s dilemma” (Christensen, 1997) because it is able to continuously invest in emerging businesses; in many ways Amazon is a startup characterized not only by volatility, but also astonishing growth potential.

Whereas most businesses have a difficult time moving into a new line of business or pursuing opportunities that are on the edge of the market, Amazon appears to seamlessly conquer one market after the other. Instead of pursuing profits, Amazon is focused on “customer obsession” (“About Amazon – Working at Amazon – Our Leadership Principles”, 2017). In fact, this foundation permeates every aspect of the company. While Apple sells a tablet at an incredible mark-up (with great success), Amazon sells its Kindle at the costs of production. Neither business model is by definition superior than the other, but to Amazon the Kindle is just another core gear that will accelerate the growth of its flywheel.

While it is true that most retailers with brick-and-mortar shops have a target on its back as the Amazon empire expands, Amazon is actually coming after numerous other sectors and markets. Recently, Amazon acquired Whole Foods, the news of which sent the grocery stocks tumbling; a perfect illustration of Amazon’s growing influence (Garcia, 2017). Yet besides supermarkets, Amazon has entered the streaming business, the newspaper business (a business typically viewed as a dying dinosaur), and, most recently, the shipping business. As Amazon announced plans to start developing its in-house logistics capabilities (Finimize, 2017b), shareholders of companies like FedEx and UPS hold their breath – Amazon is singlehandedly their biggest customer. Regardless of how the shipping story unfolds, the stocks of these companies will definitely form an interesting narrative in the years to come. How will traditional, legacy shipping companies respond with the knowledge of Amazon’s retail disruption? Is there anything they can do?

Also, do you think Amazon competes with Netflix? In some ways, I think yes. In many ways, I think no. Though not as popular in the Netherlands, people in the US tend to subscribe to both products. The flywheel that Amazon has built means that Amazon Prime and Netflix are not substitutes for one another. Sure, these companies compete with one another on the supply side and bid against each other, but on the demand side, consumers are willing to pay for both services. Again, the flywheel can be observed here too. Based on data, Amazon knows that when consumers begin to use one of their services, there is a huge incentive for them to use one of their other services. Since consumers want to get the most value out of their prime membership, they will even feel inclined to use Prime Video even though they may also have a running Netflix account. Underneath it all, because Amazon has this unusual way to monetize the premium content, Amazon is able to charge less for the premium content than they otherwise would have to charge if they did not have the flywheel to drive sales in the other branches.

I cannot help but be impressed at how an online bookstore has grown to the company it is today with so much to offer and yet so much more innovate in the years to come. I believe that the Amazon narrative should not focus on the markets that are being disrupted by this tech giant, but rather on which markets will survive the entry of this forward-thinking, flywheel-driven conquering business machine.

References

About Amazon – Working at Amazon – Our Leadership Principles. (2017). Amazon.com. Retrieved 11 October 2017, from https://www.amazon.com/p/feature/p34qgjcv93n37yd

Christensen, C. (1997). The innovator’s dilemma (1st ed.). New York, NY: Collins Business Essentials.

Finimize. (2017a). ? The EU slaps Amazon. Finimize. Retrieved 11 October 2017, from http://us10.campaign-archive2.com/?e=ac7f20ffb4&u=fd92d4d6912bf051aceebbc27&id=b383a5b04c

Finimize. (2017b). ? Your Amazon delivery has arrived. Finimize. Retrieved 11 October 2017, from http://us10.campaign-archive.com/?e=ac7f20ffb4&u=fd92d4d6912bf051aceebbc27&id=21e6a20021

Garcia, T. (2017). Grocery retail stocks battered after Amazon-Whole Foods announcement. MarketWatch. Retrieved 11 October 2017, from http://www.marketwatch.com/story/grocery-retail-stocks-battered-after-amazonwhole-foods-announcement-2017-08-24

Gensler, L. (2017). Toys ‘R’ Us Files For Bankruptcy, But Will Keep Stores Open. Forbes.com. Retrieved 11 October 2017, from https://www.forbes.com/sites/laurengensler/2017/09/19/toys-r-us-bankruptcy/#aba4fe1574ae

Malone, T., Yates, J., & Benjamin, R. (1987). Electronic markets and electronic hierarchies. Communications Of The ACM, 30(6), 484-497. http://dx.doi.org/10.1145/214762.214766

Schrage, M. (2017). For a Return on Platform Investment, Focus on New Capabilities. MIT Slogan Management Review.

Seely, S. (2017). The Amazon Flywheel: Part 1. Sam Seely Blog. Retrieved 11 October 2017, from http://www.samseely.com/blog/2016/5/2/the-amazon-flywheel-part-1

Stone, B. (2013). The Everything Store: Jeff Bezos and the Age of Amazon. Little, Brown and Company.