Once a disruptor to Blockbuster and other video rental firms, Netflix started as a cheaper, simpler way to watch your favourite movies and TV shows. Then, utilizing on-demand video streaming, they started competing with cable networks as well.

According to Christensen, Netflix is a classic case of disruptive innovation. Netflix entered the streaming market at the bottom as an inferior product. They had a limited catalog and lower bitrates, but had success with consumers who were both fed up with cable networks’ prices and their complexity, and did not want to turn to piracy or other illegal ways of watching content on the other. In fact, in the early days of streaming, Netflix made video piracy obsolete. It simply wasn’t worth the risk anymore when Netflix was so affordable. Then, slowly, as they obtained more licences and technological capabilities improved, they started winning in quality as well. The disruptor had become an incumbent itself.

Now, a decade later, the streaming landscape resembles the incumbent it displaced more than what it originally promised consumers. Fragmented supply, price increases, frequent advertisements, crackdowns on account sharing, and region-locked content have reintroduced the friction to the market that streaming originally took away.

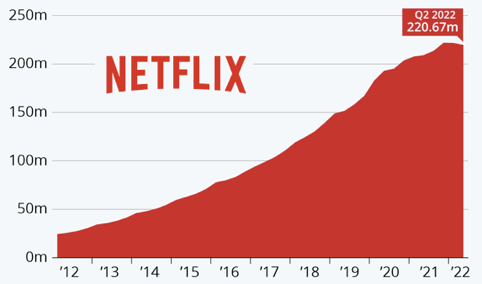

Consumers are clearly unhappy with these developments. Netflix posted its first ever subscriber decline in Q2 2022, losing over 2 million subscribers in one month (GlobalData, n.d.). While this rapid decline in subscribers was an exception, caused by Netflix’s announcement of no longer allowing password sharing, it exemplifies the issues the streaming industry currently has. But where are consumers turning now? Who is disrupting Netflix?

It turns out, video piracy sites haven’t been sleeping while Netflix has grown. They have turned to mimicking the disruptor’s playbook. They centralize the now fragmented catalogs, breaking down regional barriers, they don’t require accounts, and most importantly, they have caught up in quality as well. Modern video piracy sites not only support Full HD video streaming in real time, but their user interfaces have massively improved as well.

As they are now winning in convenience and able to compete in quality, video piracy sites are acting as a low-end aggregator in the streaming space, and they are regaining market share quickly. The US economy alone loses between $29 and 71$ million due to digital video piracy per year (Spajic, 2023).

And so the cycle continues. But where is the streaming industry going next? Netflix once disrupted the industry by making video simpler. And consumers are now asking for the same simplicity again. If streaming can once again be the most convenient way to watch your favourite movies and shows, piracy’s advantage shrinks again. So the question for Netflix and its peers is simple: How can they reclaim consumer trust and market share, without abandoning profitability?

GlobalData. (n.d.). Netflix loses almost a million subscribers in last quarter. https://www.globaldata.com/data-insights/technology–media-and-telecom/netflix-loses-almost-a-million-subscribers-in-last-quarter/

Spajic, D. J. (2023, April 10). Piracy is Back: Piracy Statistics for 2025 | DataProt. dataprot. https://dataprot.net/blog/piracy-statistics/