The rapid rise of UK-based fintech Revolut is well-documented. Founded in 2015, the company already has over 15 million users, with its services available in all EEA countries, Australia, Japan, Singapore, Switzerland and the United States (Revolut, 2021a). Revolut’s initial value proposition was centered around two key pillars: its fully digital and lightning-quick onboarding and services, enabled by the customer-friendly mobile application, and the ability to instantly exchange currencies at very advantageous rates using the application’s ‘multi-currency wallet’ (Crow and Megaw, 2020).

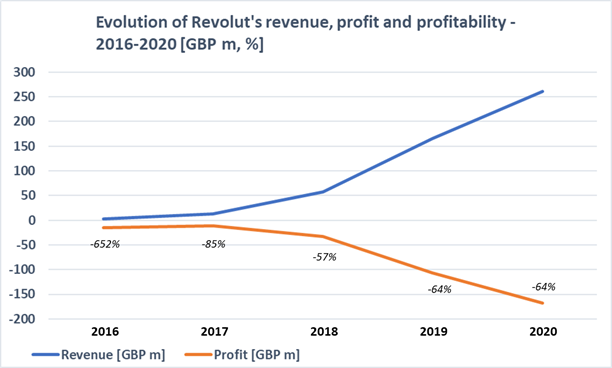

However, since the company’s launch, its ability to reach profitability has been considered questionable (Detrixhe, 2019). This was given by the intensity of the competition, coming from similar players (e.g., Monzo, Monese) and from incumbent banks accelerating their processes of digital transformation, and by the low-margins sources of revenue characterizing the initial iterations of Revolut’s product. While registering strong user base and revenue growth, Revolut’s losses continued to mount:

Over the past 12 months, though, the fintech’s ‘weapon’ for becoming profitable and winning in the market became apparent: network effects. Network effects, or externalities, can be defined as the change occurring in the value of a product or service due to the increase in the number of consumers using it in a shared way (Eisenmann, Parker and Van Alstyne, 2006). They can be either positive (i.e., the value of the product/ service increasing with the number of users) or negative and their influence can be felt on the ‘same-side’ (i.e., the value of the product/ service changes for one group of users when the number of users within that group is changing) or ‘cross-side’ (i.e., the value of the product/ service changes for one group of users when the number of users of a parallel group employing the product/ service is changing).

In Revolut’s case, positive same-side network effects were at the core of their spectacular user base growth. More specifically, as the number of users rose, the value of Revolut’s offering increased for all customers due to the ability to conduct instant, fee-less transactions with more and more people, using a growing number of currencies. This was further enhanced by the implementation of attractive referral schemes, with €5-10 rewards available for existing customers for each new user brought to the platform (Revolut, 2021b). As the user base gained critical mass, the company was able to start segmenting their customers and implement versioning, offering different packages of extra services (e.g., metal physical cards, access to airport lounges throughout the world, etc.) on top of their free offerings for various monthly subscription fees.

While the subscription plans quickly became a key revenue source, accounting for ~30% of Revolut’s income in 2020 (Woodford, 2021), it seems that leveraging same-side network effects was just the first step in the company’s path to profitability. In July 2021, Revolut announced the rollout of the ‘Revolut Stays’ service for its UK users, effectively entering the online travel market (Blew, 2021). Revolut customers can now book holidays all over the world at accommodation providers integrated in the application, even receiving 10% cashback on their booking costs if they are subscribed to one of the more expensive paid plans. The implications of this move are significant, as it signals the company’s likely strategy going forward: creating positive cross-side network effects to generate new and more profitable revenue sources, on the path to potentially becoming a ‘super-app’ such as WeChat in the Chinese market.

In this specific case, Revolut comes with a highly attractive value proposition for accommodation providers, namely a customer base already larger than 15 million. To put it into context, Expedia, the 2nd largest player in Europe has ~20 million customers, with a market share of 13% (Statista, 2021). As the number of users will grow further, more and more accommodation providers will want to be part of Revolut Stays, in order to get access to them. And as the offering on Revolut Stays becomes more diversified, the number of Revolut users itself will be further boosted by travelers looking for the best options available. This ‘virtuous circle’ is replicable with other segments of the travel industry, such as flights booking, car renting and insurance, with Revolut indeed announcing it plans to start offering these services as well in the near future (Browne, 2021).

From hereon, the opportunities become endless: if one can conduct all banking operations and fulfil their leisure travel needs from one application, at the highest possible convenience, why not also order a ride from it while on holiday? Or find a restaurant, book a place in advance and confirm it with a down payment? Or even use it to chat with the new friends made during the holiday? As WeChat’s model has proven in China, the significant impact of the network effects and the convenience factor can make it possible for just one application to go to the status of ‘super-app’, allowing users to conduct most of their day-to-day activities within no more than 5 screens, while reaching record levels of profitability (BBC, 2018).

Whether replicating a similarly far-reaching model is possible in markets such as Europe or the US, where competition in all segments is much stiffer, remains doubtful. However, Revolut’s continually growing user base will certainly represent a more and more attractive proposition for players across multiple industries, allowing it to unlock new sources of positive cross-side network effects. Over time, these are likely to turn Revolut into a profitable business and make it one of the major players in today’s growing platform economy.

References

BBC, 2018. WeChat’s owner Tencent sees profits soar by more than 60%. BBC News. Available at: https://www.bbc.com/news/business-44149371 (Accessed: October 8, 2021)

Blew, G. (2021). There’s a new way to book your perfect stay. Revolut Blog. Available at: https://blog.revolut.com/say-hello-to-stays/ (Accessed: October 8, 2021)

Browne, R. (2021). Revolut, Europe’s $33 billion fintech giant, launches a travel booking feature. CNBC. Available at: https://www.cnbc.com/2021/07/20/revolut-launches-travel-booking-feature-stays.html (Accessed: October 8, 2021)

Crow, D. and Megaw, N. (2020). Revolut is the most hyped fintech in Europe. Can it grow up? FT Magazine. Available at: https://www.ft.com/content/7fa2a8ea-8e66-11ea-a8ec-961a33ba80aa (Accessed: October 8, 2021)

Curry, D. (2021). Revolut Revenue and Usage Statistics. Business of Apps. Available at: https://www.businessofapps.com/data/revolut-statistics/ (Accessed: October 8, 2021)

Detrixhe, J. (2019). Digital banks are racking up users, but will they ever make money? Quartz. Available at: https://qz.com/1679197/when-will-digital-banks-like-n26-and-revolut-start-making-money/ (Accessed: October 8, 2021)

Eisenmann, T., Parker, G. and Van Alstyne, M. (2006). “Strategies for Two-Sided Markets”. Harvard Business Review, 84(10). Available at: https://hbr.org/2006/10/strategies-for-two-sided-markets (Accessed: October 8, 2021)

Revolut, 2021a. What countries are supported. Revolut. Available at: https://www.revolut.com/en-BE/help/profile-plan/verifying-identity/what-countries-are-supported (Accessed: October 8, 2021)

Revolut, 2021b. Referral campaigns. Revolut. Available at: https://www.revolut.com/en-NL/help/more/2021-referrals-campaign (Accessed: October 8, 2021)

Statista, 2021. Number of users in the Online Travel Booking market in Europe* from 2017 to 2023. Statista. Available at: https://www.statista.com/forecasts/891338/number-of-users-in-the-online-travel-booking-market-in-europe (Accessed: October 8, 2021)

Woodford, I. (2021). Losses at Revolut double to £207m as revenue growth slows. Sifted. Available at: https://sifted.eu/articles/revolut-losses-results-2020/ (Accessed: October 8, 2021)